The tide is turning in Africa

Negative news coverage from Africa is overshadowing a surprisingly positive trend developing across the continent

It’s now been more than a decade since the Africa Rising narrative emerged. The excitement over Africa’s prospects drew a flood of international investors looking for opportunities on the continent—and dissolved into despair as markets deteriorated and opportunities evaporated.

But while the newsflow from Africa is still resolutely negative, focusing on coups, natural disasters and conflict, we’re seeing a stream—or actually, a fast-flowing river—of positive developments across the continent in 2024.

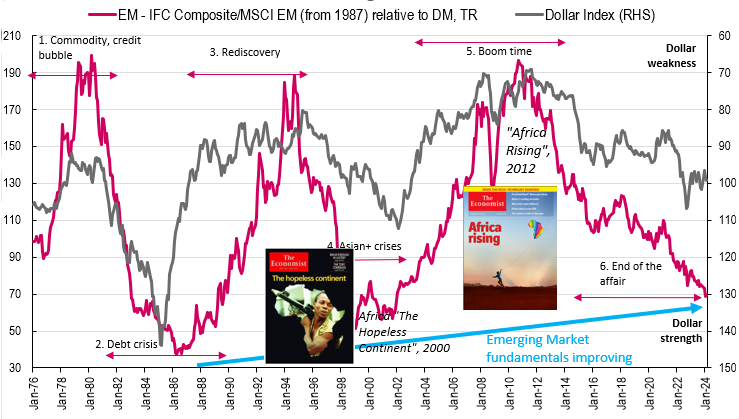

Investors haven’t caught up yet. A chart of EM equities vs DM equities (the red line below) shows we’re nearly back to the lows that prompted the Economist to dub Africa “The Hopeless Continent” in the year 2000. That suggests many markets have priced in all the bad news, but not much of this flow of good news.

But the good news is emerging in all corners of the continent.

South Africa has a new coalition government that is likely to push ahead with much-needed pro-growth reforms. While I feared the long-ruling ANC party would not make this choice, I now believe there is a decent case for South Africa’s GDP to start rising at 3% a year instead of the 1% the IMF has been expecting.

Egypt and Nigeria have delivered currency reforms that make their currencies about the cheapest in the world on my REER model—30% undervalued to their long-term history.

South Africa, Egypt and Nigeria are basically the biggest economies in Africa, so when it’s all going wrong in those countries, it sends a very negative signal. The change in outlook is a big deal.

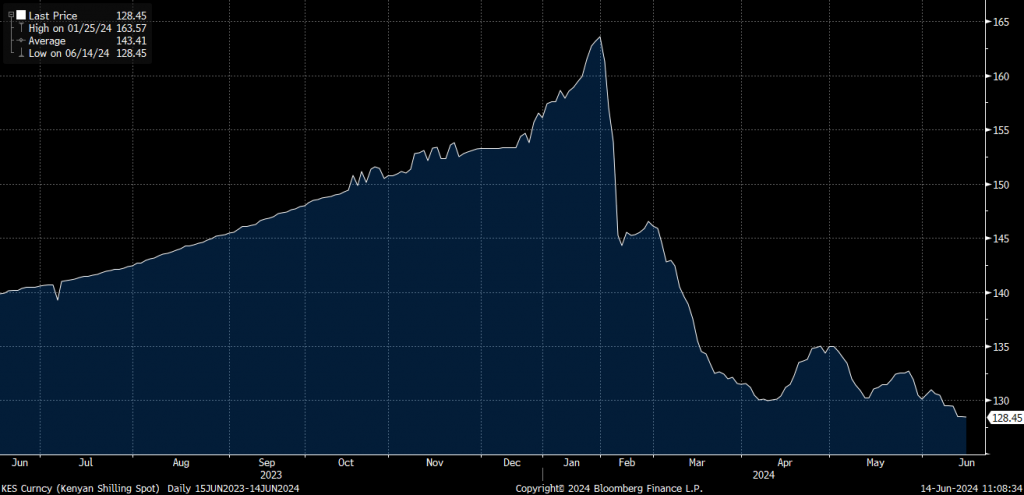

Kenya, another relative giant on the continent, is slashing its budget deficit from nearly 6% of GDP to 3% of GDP in the budget recently presented put to parliament. This has triggered protests, and promises to adjust the budget (fewer tax hikes, less spending) but the broad direction is still positive. Its currency is one of the strongest performers against the US dollar in the world this year.

In far West Africa, Senegal saw contested elections earlier this year, and a misstep by the then-President Macky Sall prompted concerns that the country, which has long been considered a beacon of democracy in the region, was heading down a different path. Sall quickly resolved the situation and the opposition, which won the election on a populist platform, is now showing itself to be more pragmatic.

Senegal will be one of the fastest growing economies in the world in 2024-25 with around 7-10% growth.

Angola is continuing hard subsidy reforms as it tries to diversify its economy.

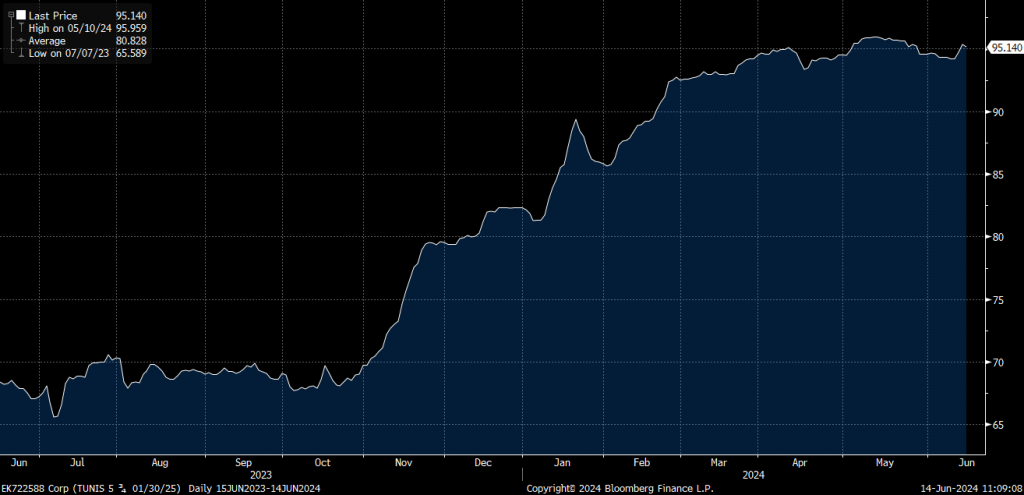

Countries like Tunisia have avoided default, and even Zimbabwe has introduced (another) currency to get inflation down.

Zambia has found agreement on its debt restructuring. Ethiopia and Ghana should follow later in the year.

Ethiopia is about to IPO 10% of its telecom company in what will be de facto launch of popular capitalism in the country. I expect an IMF backed reform package to come within months involving currency, interest rate and fiscal reforms.

Reaction time

Equity investors seem barely to noticed this flood of good news. In fact—perhaps ironically—Blackrock decided this month to shut down its Frontier ETF, after struggling with all the FX issues that beset markets such as Nigeria and Egypt in recent years.

Debt markets though have loved the story. And while still providing a high return in US dollars, they now give us a high return in local currency trades too, most obviously in Egypt.

I’ve not seen such a stream of positive developments on the continent in at least a decade. Of course this has come just two years after I’ve published The Time Travelling Economist, which explains the underlying structural challenges that have contributed to the past decade of poor performance.

And this doesn’t mean that people on the ground are better off today. In fact, it’s the reverse, with devaluation and tax rises undoubtedly making many feel this is the worst year they’ve experienced in a long time.

But we now have real reasons to believe that economies can recover, via export growth, improved current accounts and lower interest rates in the coming years, and via economic reforms that help businesses and households work effectively.

A truly remarkable year is unfolding.

Read next

Emerging economies face a jobless boom

Foreign investment flatters growth statistics, but its shrinking impact on employment leaves emerging markets vulnerable

History may be about to repeat itself in Argentina

Embattled president turns to external financing, but former president Macri's saga shows investor confidence can be fleeting

Mid-term report card on Saudi Arabia’s Vision 2030: ‘Could do better’

London-based consultancy Capital Economics says the much-publicized frustrations of Saudi Arabia’s ambitious Vision 2030 strategy are balanced by some solid successes

China ramps up EM investments as tariff risks reorder market opportunities

EM asset performance reverses as Chinese companies hedge against Trump tariff risks