By Ken Stibler, Noah Berman and Dan Keeler

Welcome to the latest edition of Frontier Markets News. As always, I would love to hear from you at dan@frontiermarkets.co with news ideas, feedback and anything else you find interesting.

If you’d like to receive this newsletter in your inbox every weekend, sign up at FrontierMarkets.co. Please also share this link with any friends or colleagues you think would enjoy it.

Africa

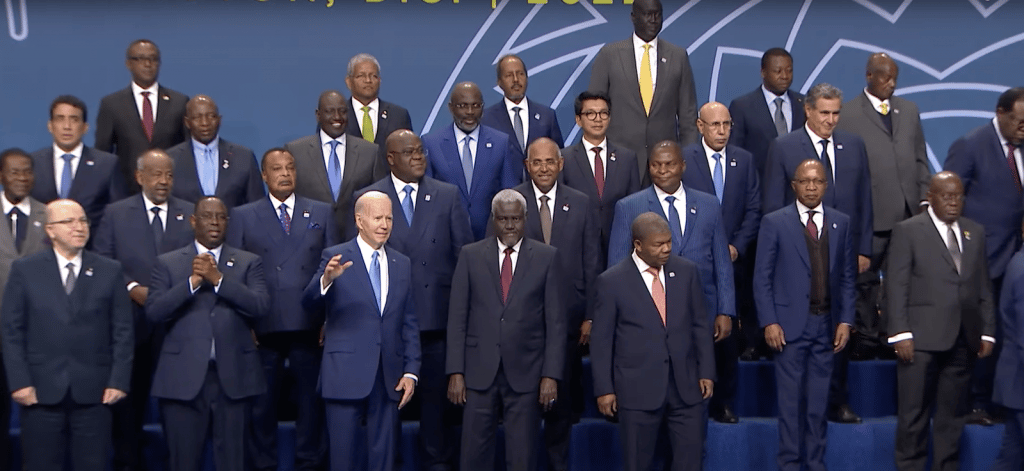

Biden stacks up commitments to Africa at DC summit. At the second US-Africa leadership summit in Washington DC this week, President Joe Biden promised a wave of investment in the continent topping $50 billion over the next three years. Among them was a $75 million to pledge to support political governance in an attempt to counter what he described as “democratic backsliding.”

The effort is timely: Since 2017, 13 of the 14 coups recorded globally have been in Africa, according to the BBC. Biden said the US will work with African governments, regional institutions and civil society to“strengthen transparent, accountable governance facilities, facilitating voter registration [and] constitutional reform.”

Mo Ibrahim, founder of the Mo Ibrahim Foundation and creator of the Ibrahim Prize for African Leadership, welcomed the initiative, but suggested its impact could be limited by the amount of funding committed. “There has been a lot of tightening of the space for civil society in Africa, so it’s important that they’re acknowledging the importance of governance, but $75 million is not enough,” he said in an interview with FMN. “There are 54 countries and they have $50 billion to give—there must be scope for more than that for governance.”

Biden’s pledge to invest at least $55 billion in Africa over the next three years also came under scrutiny as much of the funding will come from previously announced programs, Reuters reports. Nearly $20 billion will go to supporting health programs in the region, including over $11.5 billion to combat HIV/AIDS. Adult HIV prevalence remains stubbornly high at 9% in sub-Saharan Africa, according to the Population Reference Bureau.

Read the full story at FrontierMarkets.co.

‘Uncertain finances’ prompt Kenya rating cut. Kenya suffered twin difficulties this week, as a rating downgrade was quickly followed by charges that the president’s daughter had misused public funds.

Ratings firm Fitch downgraded Kenya’s issuer default rating on Wednesday, citing persistent domestic and external deficits, a high debt load and low liquidity. The rating cut for Kenya, which has long been a bulwark of financial stability in the region, may portend further turbulence for frontier economies. Across the continent, governments are facing heavy debt servicing loads, depreciating local currencies and dwindling foreign reserves.

President William Ruto’s troubles deepened with the news that his daughter Charlene Ruto may have used taxpayer money to fund an organization she created called the “Office of the First Daughter,” BBC reports. There is no such office in Kenyan law, but the younger Ruto has held numerous meetings under the title. She has denied using public funds.

Ghana reaches provisional IMF agreement. Ghana on Monday reached an agreement with the IMF to obtain a $3 billion loan, bringing to a conclusion negotiations with the international lender that began in July. Ghana signed the IMF deal after asking local bondholders to accept losses on their coupon payments, while stopping short of reducing the value of their principal investments, Bloomberg reports.

Accra reportedly will ask external bondholders to accept haircuts of up to 30% in addition to losses of coupon payments.

The deal is a staff level agreement, subject to approval by the IMF board, which is likely to approve the loan only if Ghana successfully restructures its debt with existing private and foreign government creditors, the FT reports. The restructuring is shaping up to be no easy task, with negotiations that began last month so far having yielded slow progress.

Ghana had over $36 billion in total external debt at the end of 2021, according to the World Bank. Its next dollar-denominated bond matures in July 2023.

Asia

Vietnam to cut coal use. A group of wealthy countries agreed this week to provide $15.5 billion to help Vietnam decrease its reliance on coal, the British foreign service office announced. The arrangement is the latest development in negotiations that intensified at last month’s COP27 climate conference in Sharm el-Sheikh, Egypt.

EU negotiators had failed to clinch a deal with Vietnam at the conference, where they reportedly offered $11 billion in financing. Vietnam made waves when it later announced it would in fact increase its coal power target for 2030.

As part of the new deal, signed on the sidelines of the EU-ASEAN summit in Brussels, Vietnam will peak its greenhouse gas emissions by 2030, five years sooner than its current projection. The financing package includes $7.75 billion in public funding and a matching amount in private funds from American, European and APAC banks. The money will become available over the next three to five years.

The deal follows similar agreements with South Africa and Indonesia.

‘Tech glitches’ cast shadow over Fiji election. Voters took to the polls on Wednesday in Fiji’s third general election since turning to democracy in 2013. The election pitted two former coup leaders against one another: current Prime Minister Josaia Voreqe Bainarama, who took power in a 2006 coup before being democratically elected in both prior elections, and opposition leader Sitiveni Rabuka, who led the country’s first coup in 1987.

Preliminary results were marked by confusion and controversy. After an initial tally showed Rabuka’s coalition with a significant lead, authorities took down the country’s election results app. When the app came back online on Thursday, Rabuka’s lead was diminished. Election supervisors said the error was caused by a “data transfer” issue, and that it did not affect the counting of votes, according to the New York Times.

After writing a letter to the country’s army and president asking for intervention, Rabuka was taken into custody for police questioning Friday, ABC News reports. By Saturday, he had been released. And on Sunday, a final vote count showed Bainimarama’s party had lost its parliamentary majority, leaving the main parties to negotiate a potential coalition.

Erdoğan rival’s presidential hopes fade with conviction for ‘insulting officials.’ Istanbul Mayor Ekrem Imamoglu, a politician whom polls have shown would likely dislodge Turkish autocrat Recep Tayyip Erdoğan from the presidency should he be nominated to run against him in the 2023 Turkish elections, was on December 14 sentenced to jail for insulting public officials in a speech, BNE Intellinews reports. Although Erdoğan has denied being involved in the decision to charge Imamoglu, if the conviction is upheld it would extinguish any hopes the Istanbul mayor has of competing for the presidency because he would also be barred from holding public office.

The case is based on comments Imamoglu made after his victory in the 2019 Istanbul mayoral election was annulled following complaints by Erdoğan’s Justice and Development Party. Imamoğlu said the people who cancelled the electons were “fools,” an assertion voters seemed to agree with, as they gave him a landslide victory when the poll was repeated.

Tens of thousands of supporters gathered in central Istanbul on Thursday to protest against the sentence, and the US State Department said it was “deeply troubled and disappointed” by the potential removal of one of Erdoğan’s biggest rivals from the political scene, Dawn reports.

Middle East

Iran protests ‘create lasting challenge to government.’ Western and Middle East security officials have concluded that a three-month-old Iranian protest movement represents a lasting drive for change that will challenge the foundations of the Islamic Republic, Dov Lieber reports in the Wall Street Journal. The security officials said the protest movement’s durability was surprising, given how quickly the Iranian government put down demonstrations in 2009, 2017 and 2019.

Protests erupted in September after the death of a young woman detained for allegedly violating Iran’s female dress code and quickly transformed into demands for the end of the Islamic system that has ruled the country for 43 years. Israeli officials said they believe the unrest is likely to continue because protesters are focused fully on human rights and freedoms, rather than on economic anxieties.

The Biden administration has publicly hailed the Iranian protesters as heroes, but US and Israeli officials said a lack of unifying leadership was diluting the impact of the movement. That sentiment is also shared by some European officials based in Tehran, who have told diplomats that the Iranian government isn’t at risk of being toppled soon by the protests.

Europe

Hungary unblocks EU agenda in exchange for badly needed ‘recovery funds.’ Hungary and the EU struck a complex political deal to lift Budapest’s veto on aid to Ukraine and a minimum effective tax rate in exchange for unblocking recovery funds, the FT’s Sam Fleming and Valentina Pop write. The dispute centered on Hungary’s longstanding inability to access €5.8 billion in EU recovery funding because of European Commission concerns over corruption and democratic backsliding.

At the same time, though, member states have decided to freeze €6.3bn of so-called cohesion funding to Hungary after the commission found early this month that Budapest had failed to deliver rule-of-law reforms needed to access the funding. This week’s agreement saw Budapest agree to integrate the rule-of-law reforms into Hungary’s recovery plan, with access to EU funding dependent upon its reaching key milestones.

The decision by Hungary’s prime minister Viktor Orbán to end the yearslong dispute underscores the country’s urgent need for EU funding. Investor concern over Hungary’s access to EU funds had triggered a painful sell-off in the forint, which fell 11% against the euro this year, despite Hungary having the EU’s highest interest rate at 18%.

Latin America

Latin American leaders splinter over Peru ‘coup’ as protests intensify. Peru’s political drama intensified this week after it appeared the country had calmly dealt with ousted president Pedro Castillo’s attempted coup. While the nation’s institutions largely responded quickly and in unison to transfer power and secure the capital’s security, the effective transfer is now being challenged by sweeping protests across the country, especially in rural areas where Castillo drew his stronger support.

So far, protests have closed down highways and airports, leading Castillo’s replacement, President Boluarte, to institute a state of emergency and direct the military to secure key infrastructure. To complicate the political dynamics on the streets, other leftist leaders across the region refused to recognize Boluarte as president of Peru. The governments of Colombia, Mexico, Argentina and Bolivia called for Castillo’s return, while Boluarte has received the backing of Chile, Ecuador, Uruguay and Costa Rica.

The deteriorating security and political situation in Peru threatens to erode investor and business sentiment, which has hitherto helped fuel Peru’s rapid economic growth, even in the face of long-standing political instability. Despite markets’ reacting poorly to the current protests, though, a strong, independent central bank has ensured macroeconomic stability before amid similar political crises.

Chile moves to re-rewrite the constitution, but the effort brings political risks. Chile’s main political parties revived efforts to rewrite the constitution this week, agreeing to draft a new charter through a constitutional council of experts and elected officials, Bloomberg’s Valentina Fuentes reports. The new push to replace the dictatorship-era constitution comes after a disastrous rejection in September’s referendum after left-wing delegates caused fears that the document would undermine growth and erode checks on power.

Despite September’s failure, almost 70% of Chileans still want a new constitution. The new process will be much more technocratic than the last, incorporating veto points at both chambers of congress, a 2/3 vote required to include articles, as well as a final plebiscite in late 2023.

In their agreement, the parties established that any new constitution would enshrine basic principles including the protection of nature, central bank independence, private property and indigenous rights. The market response was muted and observers were generally optimistic about the new effort, which is seen as crucial for Chile’s President Gabriel Boric.

Global

Frontier countries consider adopting rupee. Some frontier markets, including Tajikistan, Cuba, and Sudan, have indicated an interest in adopting a trade settlement mechanism denominated in Indian rupees, Reuters reports.

The system, set up by the Reserve Bank of India (RBI) in July, has gained traction since sanctions spurred by the Russian invasion of Ukraine made transacting in US dollars difficult. Russia has already used the rupee settlement system to facilitate its sale of oil to the South Asian country.

India is eyeing governments with a shortage of dollars in their foreign reserves as potential candidates for the system, according to Reuters. Mauritius and Sri Lanka have already been approved by the RBI to transact in rupee-denominated accounts. Meanwhile, central bankers in India have held talks with Saudi Arabia and the UAE about setting up trade mechanisms that involve their respective currencies and cut out the US dollar.

Falling dollar raises hopes but offers mixed effects for frontier markets. Emerging markets have endured a difficult year thanks to a combination of rising interest rates, a strong US dollar and increased food and fuel prices. As the end of the year looms, though, the dollar has been weakening and US interest rate rises are slowing, offering hope for battered developing economies, according to the FT.

It is too early to assume that easing by the Fed will automatically lead to rate cuts in developing countries, however. Inflation remains high in many emerging markets, which will likely result in central banks being forced to keep interest rates high into next year, delaying any pickup in economic activity.

Despite these challenges, some analysts believe that emerging markets will eventually benefit from lower interest rates and a weaker US dollar. Although Zambia, Sri Lankaand Ghana have already defaulted, loosening external conditions might allay a wider debt crisis in vulnerable countries such as Kenya, El Salvador and Pakistan.

The Long Read

Gulf nations warm to Emerging Asia as Western alliances weaken. Heeding warnings from the IMF and others about declining demand for hydrocarbons—and reading the political tea leaves—Gulf nations are shifting their focus from West to East. In this week’s Long Read, Middle East analyst Chris Muth and FMN’s Ken Stibler break down the reasons for the warming of relations between emerging Asia and the Gulf and the prospects for the future.

Read more at FrontierMarkets.co.

What we’re reading

Egypt: Depreciating pound stokes fears about external debt, FDI. (The Africa Report)

Tunisia to elect new parliament in vote widely decried as a sham. (FT)

Sudan, UAE’s consortium sign $6-bln deal to build new port on Red Sea. (Sudan Tribune)

Rwanda secures $319 million under IMF’s new climate funding program. (Bloomberg)

Data curbs from Vietnam to Indonesia to hit trade by up to 9%: study. (Nikkei)

Cambodia’s China dependence deepens as first expressway opens. (Nikkei)

Myanmar regime fails to unseat pro-resistance UN ambassador. (Nikkei)

Bangladesh government digs in against protests as economy teeters. (Nikkei)

Bankrupt Sri Lanka holds breath for Paris Club’s China overture. (Nikkei)

In Central Asia’s wealthiest country, Kazakhstan, many can barely afford food and rent. (Radio Free Europe)

World Bank says debt increasing in Middle East countries. (Al Monitor)

Pakistan tops new index measuring Chinese influence around the world. (Radio Free Europe)

Russia replaces Iraq as top oil supplier to India in Nov. (Reuters)

Sole road connecting Nagorno-Karabakh to Armenia blocked by protesters from Azerbaijan. (Radio Free Europe)

Serbia’s president says Belgrade seeks to deescalate situation in Kosovo. (Reuters)

EU says to ’monitor’ Albania–UAE luxury port deal. (Balkaninsight)

‘Cuba is depopulating’: Largest exodus yet threatens country’s future. (NYT)

Guatemala’s authoritarian slide under Giammattei is putting Biden in a bind. (World Politics Review)

Latin America likes El Salvador president Bukele’s ’war on gangs.’ That’s a problem. (World Politics Review)

Central America sees economic boon as migrants flow through on way to US. (The Guardian)

Argentina’s populist political movement is at its lowest ebb. (The Economist)

Then and now, Argentina’s World Cup overlaps with high inflation. (Bloomberg)

Read next