By Ken Stibler, Noah Berman and Dan Keeler

Welcome to the latest edition of Frontier Markets News. As always, I would love to hear from you at dan@frontiermarkets.co with news ideas, feedback and anything else you find interesting.

If you’d like to receive this newsletter in your inbox every weekend, sign up at FrontierMarkets.co. Please also share this link with any friends or colleagues you think would enjoy it.

Africa

Peace deal in Sudan. Leaders of Sudan’s military and a group of civilian pro-democracy parties agreed to a political framework this week that is expected to speed the transition to civilian rule. The deal is expected to institute a transitional civilian government and pave the way for a new constitution.

Expectations for the transition remain measured because of the failure of similar deals in the past, Al Jazeera reports. Several grassroots and rebel groups have declined to sign on to the deal arguing that it didn’t go far enough to remove the army from power, Africanews reports.

The last version of a deal to end the country’s political power struggle between military and civilian leaders ended with a coup in October of 2021.

If implemented, the framework will establish a democratic transition within two years, with a prime minister selected by the “forces of the revolution,” the New York Times reports. The military will take a back seat in politics, joining a civilian-led security and defense council.

US to support Africa in G20. President Joe Biden is expected to announce his support for a permanent African Union presence in the G20, the Washington Post reports. He is expected to make a formal announcement at the US-Africa leaders summit in Washington next week.

Representation in the G20 has long been a goal of African states. South Africa is the only African economy currently in the G20. The African Union represents all the countries on the African continent.

African leaders have criticized international organizations for leaving them out of discussions on development, climate change and other issues even as the continent is heavily affected by international policy. African states have been disproportionately affected by the war in Ukraine, for example, which has made staples like wheat and fuel more expensive.

Support for AU membership in the G20 comes as the US attempts to counter China, which has become a major player in the region, in part through debt financing. China controlled 12% of the continent’s external debt as of 2020, according to Reuters.

Asia

Bangladesh cracks down on opposition. After a week of protests that left hundreds arrested and one dead, officials in Bangladesh announced the arrest of two senior opposition leaders on Friday. The South Asian nation, which sought a $4.5 billion IMF bailout in July to help tackle economic issues including dwindling foreign reserves, plans to host elections next year that are expected to deliver another victory for Prime Minister Sheikh Hasina, who has been in power for the past decade.

One of the politicians arrested was Mirza Fakhrul Islam Alamgir, the de facto leader of the opposition Bangladesh Nationalist Party (BNP), the New York Times.

Bangladesh has grown increasingly repressive in recent years. The previous opposition party leader, Khaleda Zia, was arrested in 2018 and thousands have been arrested under the country’s digital security law, which criminalizes offenses that can include critical comments on Facebook.

Nevertheless, citizens have grown more restless in recent months, as lingering effects from the pandemic and the war in Ukraine make imports more costly. Tensions came to a head this week, as BNP supporters clashed with police in front of the party’s office in Dhaka.

Pakistan curbs imports as it struggles to reassure IMF. Pakistan is restricting imports and trying to get an IMF bailout back on track, as it struggles to find dollars to pay a mountain of foreign debt, Saeed Shah reports in the WSJ. The country disclosed this week that its foreign-exchange reserves have dwindled to the lowest level in nearly four years, with only enough to cover about six weeks of imports.

Islamabad has been meeting bilateral lenders to enlist their help. It is seeking an emergency $3 billion loan from Saudi Arabia, Pakistani officials said this week, and continuing to work with the IMF to secure the next round of financing. Any fresh Saudi injection would be on top of a $3 billion loan that Saudi Arabia rolled over just this month.

Billions of dollars of debt payments are due in the next few months from Pakistan, which is facing a delay in the release of the next tranche of its $6.6 billion bailout from the IMF, as the lender demands a better economic plan from Islamabad. The IMF program was restarted in August after stalling over large subsidies that Pakistan introduced without the lender’s agreement.

Middle East

Middle East realigns to emerging Asia amid volatile global markets and shaky Western alliances. China concluded high level meetings with Middle Eastern leaders this week in a bilateral summit with Saudi Arabia at the Gulf-China Summit for Cooperation and Development and in the inaugural Arab-China Summit for Cooperation and Development. China’s meeting with Saudi leadership saw the kingdom upgrade the countries’ relationship, allow Huawei to provide cloud computing services, further extend energy cooperation and announce bi-yearly summits.

While the summit suggests a new strengthening of relations, cooperation has been steadily increasing in previous years through drones and missile sales, expansion of telecommunications networks and pricing some Saudi oil sales in yuan. The meeting is also a substantial snub to the US, which had failed to prevent OPEC production cuts in October.

The Beijing-Riyadh cooperation reflects a broader trend across Middle Eastern monarchies toward increased trade, defense and energy partnerships with key Asian countries as Europe and the US become less relevant and reliable partners.

See next week’s newsletter for a full analysis by FMN’s Ken Stibler and Middle East analyst Chris Muth.

Latin America

Castillo’s ‘self-coup’ fails in Peru, but political dynamics threaten continued chaos. Peru’s now-former President Pedro Castillo dissolved Congress on Wednesday in an attempt to prevent a third impeachment vote against him. In a rare show of unity, lawmakers across parties, the army, and police all rejected the move, leading to Castillo’s arrest as he was attempting to flee to the Mexican embassy.

Now facing rebellion charges, Castillo is being held in the same detention center as former president Alberto Fujimori, who successfully carried out a similar so-called self-coup to neutralize congress 30 years ago. The move makes Castillo the seventh president to be detained or charged with corruption since 2011.

The former president was quickly replaced by Vice President Dina Boluarte, who called for a political truce and asked opposition parties for time to get the country back on track. Boluarte inherits the same legislative fragmentation that has led to consistent conflict between Peru’s congress and the executive branch in recent years.

Peru, long an investor darling despite political dysfunction, initially saw currency and bond markets rattled. However, the sol surged after the impeachment. “Peru’s financial markets will suffer but won’t collapse, thanks mainly to solid domestic fundamentals,” said Andres Abadia at Pantheon Macroeconomics.

Global

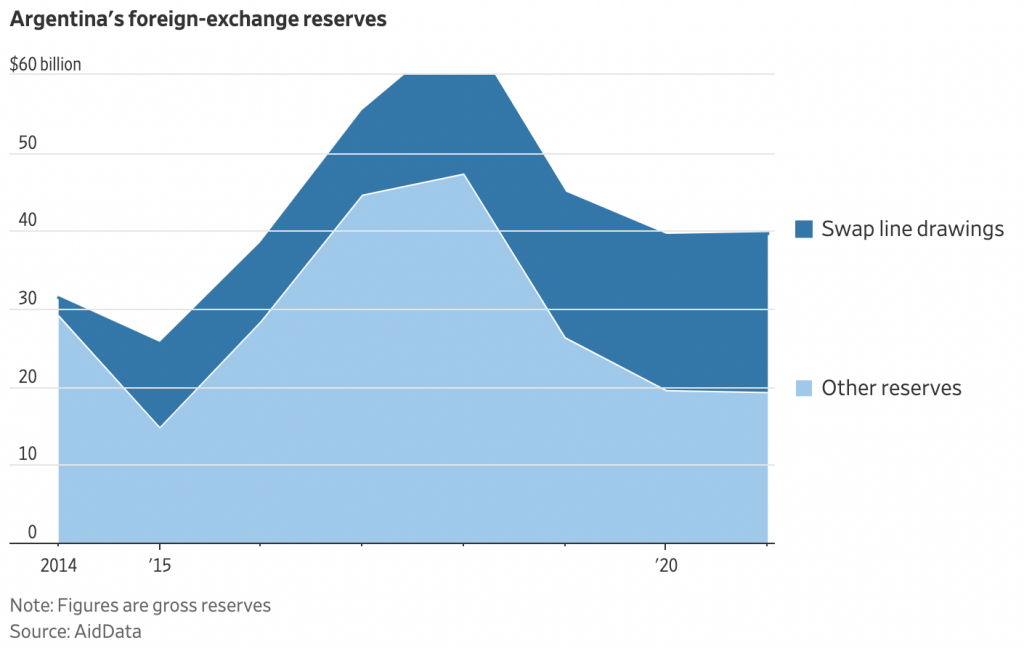

China props up Belt-and-Road borrowers via unusual channel. Hungry for foreign currency to shore up their dwindling reserves, some troubled countries have in recent years turned to the People’s Bank of China, Jason Douglas reports in the WSJ. China’s central bank has funneled billions to around 20 countries, including Pakistan, Sri Lanka, Argentina and Laos, via swap lines that allow overseas central banks to exchange their domestic currencies for Chinese yuan.

The transactions, researchers say, are part of a broad but opaque effort by Chinese authorities to prop up governments that borrowed heavily from Chinese banks as part of Beijing’s $1 trillion Belt and Road Initiative to finance infrastructure projects and win influence across the world.

By replenishing other countries’ reserves, the PBOC may be helping some of the world’s most indebted countries avoid rising borrowing costs. But economists say the swaps also help paper over problems that led to their financial troubles in the first place.

The swaps are often rolled over, sometimes for years, and researchers estimate the average interest rate for using them has been around 6% of the value drawn. The PBOC says the swap lines are there to help grease the wheels of international trade, ensure financial stability and further the adoption of the yuan in a world where trade and finance are dominated by the US dollar.

What we’re reading

Glencore to pay DR Congo $180 million to cover corruption claims. (FT)

Ghana bondholders may push against Ofori-Atta’s debt-exchange plan. (The Africa Report)

Nigeria caps ATM cash withdrawals at $45 daily to push digital payments. (Bloomberg)

Chad jails more than 260 people after mass trial over protests. (Al Jazeera)

Mozambique’s ‘hidden debt’ scandal: Ex-president’s son and 10 officials found guilty. (The Africa Report)

Egypt joins BRICS’ New Development Bank. (Mercopress)

Uzbekistan rejects Putin-proposed ‘trilateral natural gas union.’ (Radio Free Europe)

Vietnam stocks hit by recession fears and graft crackdown. (Nikkei)

Philippine businesses attack Marcos sovereign wealth fund plan. (Nikkei)

India’s Modi to skip annual Putin summit over Ukraine nuke threats. (Bloomberg)

Pakistan to buy discounted Russian oil to ease economic pains. (Nikkei)

Pakistan tops new index measuring Chinese influence around the world. (Radio Free Europe)

Thailand hits 10 million visitors in 2022 as tourism recovers. (France24)

Indonesia bans sex outside marriage. (WSJ)

Vanuatu Uses Its ‘Unimportance’ to launch big climate ideas. (NYT)

Protesters in Mongolia try to storm state palace. (Al Jazeera)

Turkey’s frustrated youth turn their back on Erdogan’s ruling AKP. (Nikkei)

UAE seeks economic pact to boost trade with war-torn Ukraine. (Bloomberg)

Russians march on foot to advance yards in bloody eastern Ukraine battle. (WSJ)

Serbian right-winger says Wagner ties could help if there’s ‘conflict in Kosovo.’ (Radio Free Europe)

Serbia mulls sending troops to Kosovo as tensions escalate. (Radio Free Europe)

Slovenia plans to build pipeline to Hungary to transport Algerian gas. (FT)

Caps on fuel prices announced to curb Argentina’s inflation. (Mercopress)

UN aid chief: Gangs control about 60% of Haiti’s capital. (AP)

Putin reported having exit plan to Venezuela if Ukraine bid fails. (Mercopress)

Argentine court sentences vice president Cristina Kirchner to six years in prison. (WSJ)

Read next